Getting on top of debt: where to begin

Debt can feel overwhelming — especially when rising living costs and repayment pressures collide. It’s not just a financial strain; it can affect your wellbeing, confidence and sense of control. But with a clear plan and steady action, it’s possible to break the cycle and move toward financial stability.

The right repayment strategy depends on your goals and circumstances. If you’re motivated by quick wins, the snowball method may suit you. If you want to minimise interest costs, the avalanche method could be more effective. And if you’re juggling multiple debts, consolidation might help simplify things.

This guide will walk you through how each method works, how to choose the right one, and how to take the first step.

Key takeaways

- Understanding your debt is the first step toward paying it off

- Choosing the right strategy can help you reduce debt faster

- Changing spending habits is essential to escaping the debt cycle

What is debt, really?

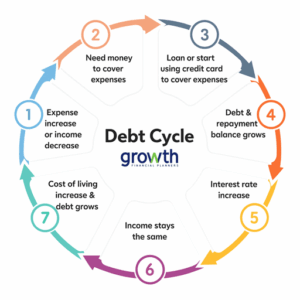

Debt is money owed — usually from loans, credit cards or other financial agreements. It can be a useful tool when managed well. Businesses use debt to grow. Families use it to buy homes or cars. But when repayments become unmanageable, debt can quickly become a burden.

Every debt comes with interest. If repayments fall behind, those costs compound. And if your expenses exceed your income, you may find yourself borrowing just to stay afloat — a pattern known as the debt cycle.

This is why it’s so important to stay aware of your debt levels, keep up with repayments, and make changes early before the cycle deepens.

Common Types of Debt in Australia

Debt is part of life for most Australians. In fact, three in four households carry some form of debt, whether it’s a mortgage, credit card, personal loan or buy-now-pay-later account. Used wisely, debt can help fund education, grow a business or buy a home. But when unmanaged, it can become a source of stress and financial strain.

1. Credit Cards

Credit card debt is the most widely held form of personal debt in Australia, with 36% of Australians carrying a balance. While convenient, credit cards often come with high interest rates — averaging 19.94% p.a. — which can quickly compound if balances aren’t paid off in full.

2. Personal Loans

Around 15% of Australians have personal loans, often used for cars, travel, education or business expenses. Car loans are especially common, with an average balance of $12,346. Student loans under the HELP scheme average $27,640, with over 3 million Australians holding education debt.

3. Buy Now, Pay Later (BNPL)

BNPL services like Afterpay and Zip are used by 23% of Australians, with an average debt of $798. While interest-free on the surface, missed payments can attract fees and lead to further borrowing.

4. Payday Loans

Used by about 5% of Australians, payday loans offer fast cash but come with steep fees. A $2,000 payday loan could cost $400 in setup fees and $80 per month, making them one of the most expensive forms of debt.

Why Paying Off Debt Quickly Matters

Paying off debt faster means less interest, more savings, and greater financial freedom. With interest rates rising, even small balances can grow quickly.

For example:

- A $5,000 credit card balance at 19.94% interest will cost nearly $997 extra over a year if unpaid.

- That’s money you could be saving, investing, or using to reduce other debts.

How to Understand Your Debt

Before choosing a repayment strategy, get clear on what you owe. Create a simple debt list that includes:

- Balance

- Minimum monthly repayment

- Due date

- Interest rate

This helps you prioritise which debts to tackle first. High-interest debts usually cost the most over time, so tracking rates is key.

You can also use tools like the MoneySmart Credit Card Calculator to estimate how long it’ll take to pay off your balance — and how much you’ll save by increasing repayments.

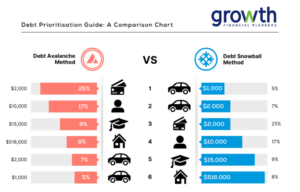

How the Debt Avalanche Method Works

With the debt avalanche approach, you begin by targeting the debt with the highest interest rate. In this example, that’s the $2,000 credit card balance. Extra repayments are directed toward this debt while minimum payments continue on all others.

Once the highest‑interest debt is cleared, attention shifts to the next most expensive debt — in this case, the personal loan — and the process continues down the list.

By tackling high‑interest debts first, you reduce the total interest paid over time. As each balance disappears, you build momentum and gradually free up more cash flow to accelerate the remaining repayments.

Debt Snowball Method

The debt snowball method takes a different approach. Instead of focusing on interest rates, you prioritise debts by smallest balance first.

You continue making minimum payments on all debts, but any extra money goes toward the smallest balance until it’s fully paid off. The quick wins create a strong psychological boost, helping you stay motivated throughout the journey.

How to use the Snowball Method:

- List debts from smallest to largest balance

- Pay minimums on all debts except the smallest

- Direct extra repayments to the smallest balance

- Once cleared, move to the next smallest

- Repeat until all debts are gone

Both strategies work — the avalanche saves more on interest, while the snowball provides faster emotional rewards. The best choice depends on what keeps you motivated and consistent.

Debt Consolidation Loans

Debt consolidation involves taking out a new loan to combine multiple debts into one. This can be helpful for people feeling overwhelmed by several repayments.

Potential benefits:

- Lower monthly repayments if the new loan has a lower interest rate

- Simplified finances with one repayment instead of many

- Improved credit score over time if repayments are made consistently

Potential drawbacks:

- Fees and charges such as establishment or early‑exit fees

- Risk of default if the new repayment still isn’t manageable

- Not a cure‑all — consolidation only works if spending habits also change

It’s important to ensure the new loan is affordable and part of a broader plan to get out of debt, not deeper into it.

Should You Save or Pay Off Debt First?

The right choice depends on your situation. High‑interest debt — especially credit cards — usually costs more than you can earn in savings, so paying it down first often makes financial sense.

However, if your debts have low interest rates and you don’t have an emergency fund, building savings may be the priority. A small buffer can prevent you from relying on credit again when unexpected expenses arise.

A clear budget and spending review will help you decide where your money is best directed.

How Much Debt Is “Too Much”?

Debt becomes a problem when it starts limiting your choices or causing financial stress. Warning signs include:

- Spending more than you earn

- Carrying credit card balances month to month

- Only making minimum repayments

- Feeling anxious about money

- Considering bankruptcy

Not all debt is bad — some can help you build wealth or reduce tax — but unmanaged debt can quickly spiral. If you’re struggling, it’s important to act early.

Services That Can Help

Support is available if you’re feeling stuck or unsure where to begin.

- Financial counselling — Free services can help you create a budget, negotiate with creditors and understand your options. The National Debt Helpline 1800 007 007 is a free service that provides Australia-trained counsellors to help you navigate and create a plan to stay on track.

- Budgeting services — Paid services such as My Budget can help you stay accountable and manage cash flow.

- Debt negotiation — Some providers can negotiate lower interest rates or fees on your behalf.

- Debt settlement — In extreme cases, creditors may accept a reduced amount, though this can affect your credit score.

- Debt recycling — With the right advice, homeowners may be able to use equity to invest and restructure debt more effectively.

Changing Your Spending Habits

A repayment strategy gives you direction, but changing the habits that created the debt is what keeps you out of the cycle long‑term. Understanding why your debt built up — whether from big purchases, day‑to‑day living costs, or small impulse buys — helps you decide what needs to shift going forward.

As you review your spending, patterns usually become clearer. Many people discover they’re overspending in one or two areas without realising it. For some, it’s small daily luxuries; for others, it’s unplanned shopping, takeaway meals, or letting subscriptions run in the background. Enjoying life is important, but when you’re working to reduce debt, being intentional about where your money goes matters.

The Role of Budgeting

A simple budget planner gives you clarity and control. Start by listing your fixed expenses using actual figures from your bank statements. These are the non‑negotiables that form your cost of living — mortgage or rent, car repayments, insurance, utilities, school fees, phone and internet, and any regular loan or credit card payments.

Next, list your variable expenses using an average amount. This includes groceries, fuel, eating out, entertainment, and every subscription or membership you pay for. Once everything is listed, separate your spending into needs and wants, then overlay your debt priorities.

This makes it easier to see where adjustments can be made. You might reduce discretionary spending, switch to a better-value internet plan, or renegotiate your mortgage rate. Even small changes free up money that can be redirected to your highest‑priority debt.

These shifts don’t just help in the short term — they build habits that prevent future debt from creeping in.

Staying Disciplined and Patient

Paying off debt takes consistency. Progress may feel slow at times, but every repayment moves you closer to financial stability. Staying committed to your plan, even when motivation dips, is what ultimately gets you to the finish line.

Tools to Support Your Budget

A structured budget template can make the process easier and help you stay accountable. Tracking your spending regularly keeps you aware of your progress and highlights areas that may need adjusting.

Bringing It All Together

Debt can feel overwhelming, but with the right strategy and mindset, it becomes manageable. When you understand your debts, seek guidance when needed, and build a budget that supports your goals, you create a clear path forward.

The avalanche and snowball methods each offer effective ways to reduce debt, and consolidation or professional support can help in more complex situations. What matters most is choosing a plan that suits your circumstances — and sticking with it.

Taking proactive steps now puts you back in control and helps you build a stronger financial future.